Destination India – Why is India a Lucrative Market for Foreign Automotive Suppliers

Estimates, Facts and Figures

According to data from SIAM, India’s total auto exports in the first quarter of fiscal 2021-22 (Q1, from April to June) was 1.4 million units, over three times the figure in the same period in the previous year. Two-wheeler manufacturers saw an especially large boost, exporting about 1.1 million units in this period, compared to 337,983 units a year ago. As the chart on the left depicts, the numbers are steadily rising to meet and overtake pre-covid levels – as can be seen from the dips through Covid and rising numbers in the 1st Quarter of FY22.

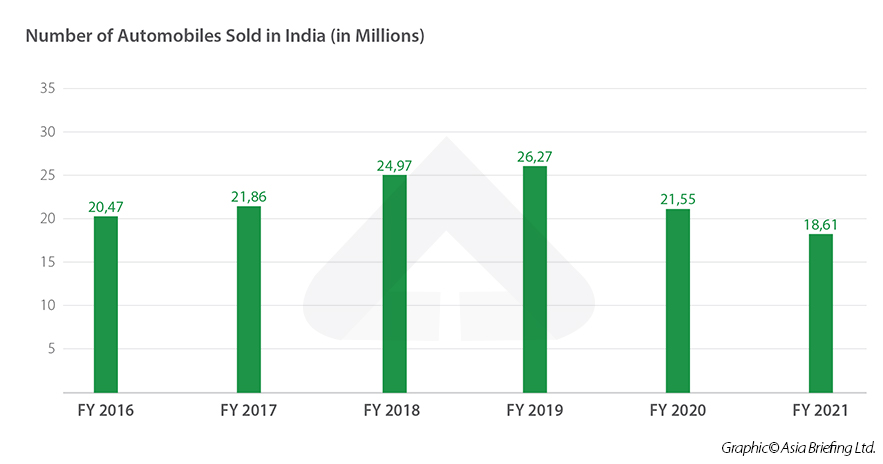

As mentioned earlier, Industry estimates the Indian automobile sector to reach US$300 billion by 2026 from the existing US$118 billion in 2020. Currently, the automotive sector contributes 7.1 percent to India’s GDP and employs a workforce of 37 million. The Automotive Mission Plan 2016-26 (AMP) envisages raising the sector’s share in GDP to 12 percent and creating employment opportunities for over 65 million people. Domestic vehicle sales for Quarter 1 of FY22 have witnessed a 113% growth over the FY21 quarter.

Status of Auto components

According to AMP 2016-26, India is expected to emerge as the 3rd largest automotive market in the world in terms of volume by 2026, after China and the USA.

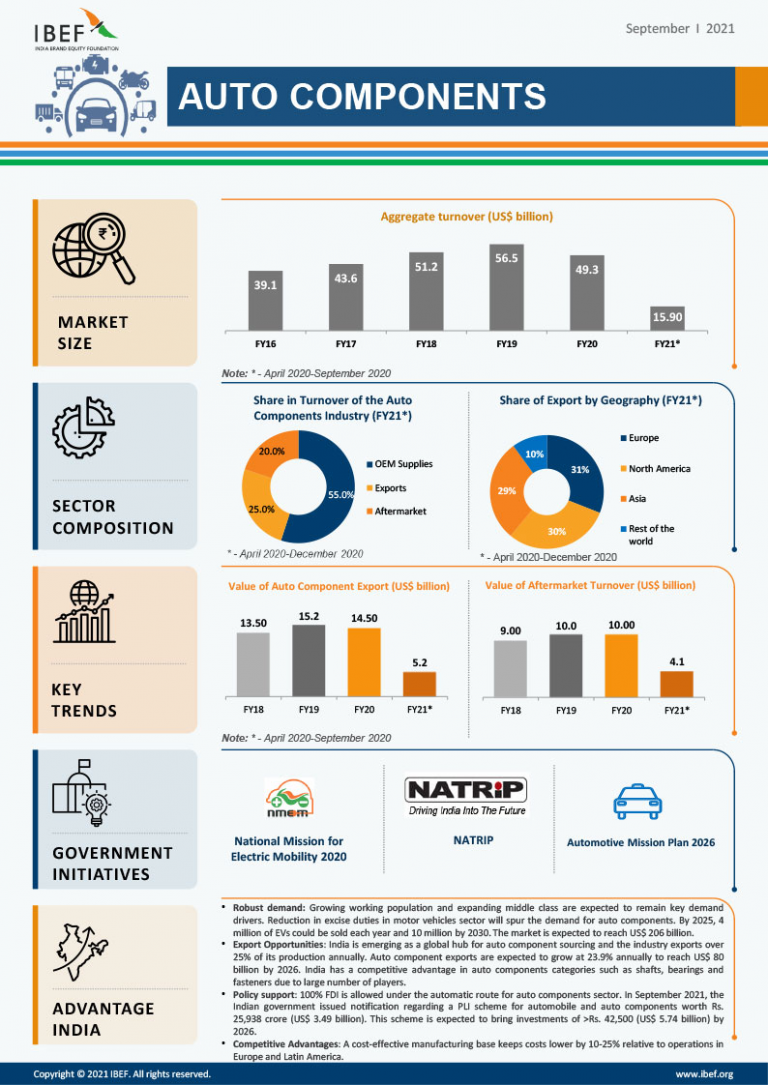

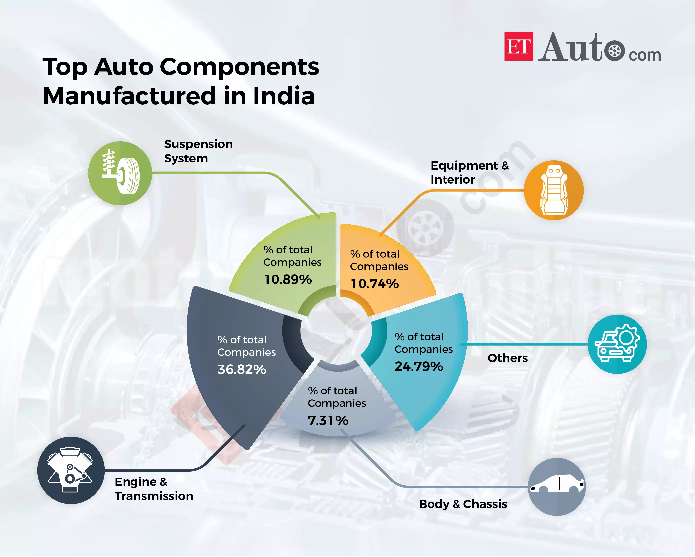

The Indian auto component industry is a critical part of the original equipment manufacturer (OEM) value chain and has grown at a healthy pace over the past few years. As per data from a report by CARE Ratings, in terms of segment-wise share in OEM supplies, the passenger vehicles segment is the largest with 45.3 percent share, followed by two-wheelers (19.6 percent share), medium and heavy commercial vehicles (12.4 percent share), LCVs (11.8 percent share), tractors (6.5 percent share), three-wheelers (3.3 percent share), and construction equipment (1.1 percent share).

Among key challenges faced by Indian component manufacturers is the low-level of technology penetration and negligible R&D capacity. According to an ICRA report released in September 2021, while the long-term growth drivers look resilient, short-term challenges like commodity inflation and semiconductor shortage persist.

{kind=link}